Trading Volume: Defined

Trading Volume is the number assets (stocks, currency, etc.) being bought and sold over a period of time. Volume can be separated into “buy volume” (also known as “ask volume”) and “bid volume” (also known as “sell volume”).

Because assets are bought and sold by many thousands of investors, there isn’t a single price, instead there’s a range of prices:

- Some sellers hope to sell quickly at $5,000 and others hope to sell more profitably at $6,000.

- Some buyers hope to buy immediately at $5,000 and other buyers hope to buy more affordably at $4,000.

When an asset has a lot of buy volume also known as ask volume, it means there are many, many buyers who want to purchase and are will to pay high prices. They will start purchasing at the lowest selling price, followed by the next higher selling price, followed by the next higher selling price, followed by the next higher… In other words, a lot of buy/ask volume results in higher prices.

When an asset has a lot of sell volume also known as bid volume, it means there are many, many sellers who are willing to sell at low prices just to get rid of their assets. They will start selling at the highest purchasing price, followed by the next lower purchasing price, followed by the next lower purchasing price, followed by the next lower… In other words, a lot of sell/bid volume results in lower prices.

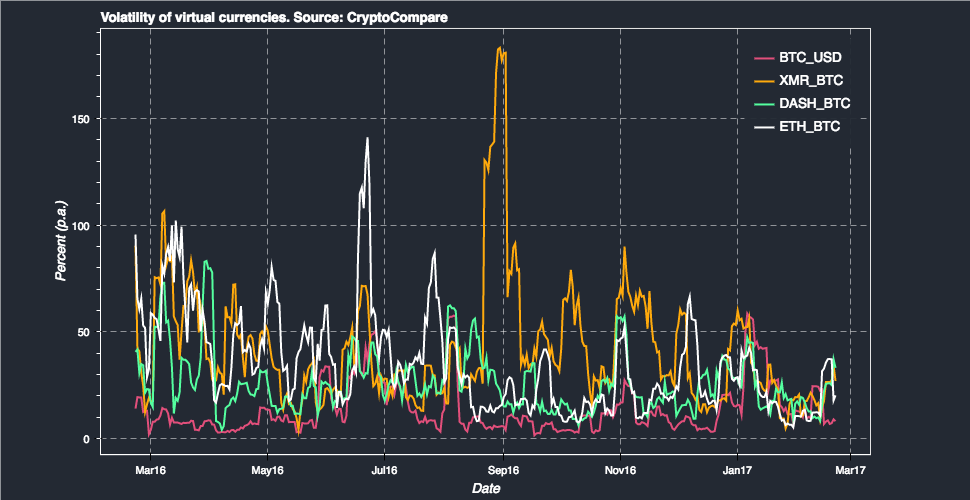

UNDERSTANDING CRYPTOCURRENCY TRADING VOLUME

Along with circulating supply and market capitalization, volume is one of the most prominent metrics in crypto. Within our premium, members-only Coinist Insiders Network, our job is to identify early stage cryptocurrencies with a high probability for success before there is any retail hype around them. We look at a coin’s trading volume before we decide to shortlist a project for further analysis. Below we’ll break down why trading volume is such an important metric when analyzing cryptos and how it can help you show a coin’s direction.

The volume of a token listed on CoinMarketCap is quite simple. It’s the amount of the coin that has been traded in the last 24 hours. For example, roughly $3.5 billion worth of Bitcoin has changed hands in the last day. You can break this down in a variety of ways; you could also list it as 3,039,787,668 Euros. Or, in crypto terms, 642,566 Bitcoins. You can also slice and dice it by exchange. In the last 24 hours, roughly 14.97% of all Bitcoin traded moved through Bitfinex, where the price is $5514 as of writing. Essentially, volume underscores how many people are buying and selling the coin. If the price of Bitcoin goes up and it shows a hefty volume, that tells us lots of people are making moves. Thus, it will likely keep going up. If the price of Bitcoin drops, but there’s minimal volume, that could tell us only a small amount of people back the trend. Let’s go into more detail on the ramifications.

Volume is arguably the most important metric for a cryptocurrency, because of the amount of ways it can be broken down. From volume, you can infer the direction and movements of a coin. It’s an essential metric for traders. Volume can examined in minute detail. You can track volume on CoinMarketCap by the last 24 hours, last week, or last 30 days. This helps reveal if a coin’s recent swings are an aberration or the norm. A coin with frequent heavy movements won’t attract attention if it has high volume. If a coin normally has less volume, heavy trading in the last 24 hours could indicate there’s some support behind the move it may be making.

You can also examine which exchanges had what volume. This matters because exchanges frequently have different prices. As well, many exchanges are geographically-focused. Kraken, for instance, is largely a European exchange. OKCoin functioned in China until the People’s Bank of China cracked down recently. Volume by exchange can reveal where the buyers or sellers of a coin are. CoinMarketCap does not, however, reflect exchanges with no fees. Exchanges that don’t charge a fee allow traders and bots to send coins back and forth for free, imitating a high volume.

Generally, the biggest and most popular coins are traded the most. If you sort by volume on CoinMarketCap, the top three coins are Bitcoin, Etherum, and Ripple, also the three largest market caps. No surprises there. But if you slide down a bit, you’ll see MonaCoin, a lesser-known currency, having higher trading volume than big names like Neo and Dash. MonaCoin isn’t much talked about, but it’s seen a remarkable 86.97% change in the last 24 hours. Coupled with a high trading volume, that’ll attract plenty of attention.

Comparatively, if we sort by lowest 24 hour trading volume in the top 100, Dentacoin pops up. It’s seen a 26.25% increase in the last 24 hours. That looks great on paper. But the low volume could make investors cautious. It might mean that the move won’t last, and that Dentacoin could soon see a correction. Of course, there’s no way to know for certain. Comparing the 1 day volume to the 7 day volume is another way we can read trends. Around $3.6 billion of Bitcoin was traded in the last 24 hours. Around $12.3 billion Bitcoin moved total in the last seven days. Almost a quarter of Bitcoin’s 7 day volume occurred yesterday. This tells us that yesterday was a massive trading day, which isn’t likely to repeat. On the other hand, you truly never know in crypto.

Cryptocurrencies are so different from established securities that there’s limited usefulness in comparing metrics. Since tokens don’t produce financial statements, they have relatively few metrics to start with. But we’ll compare cryptocurrency trading volumes to provide a sense of scale. In the last 24 hours, around $3.6 billion of Bitcoin was traded, as the price hit all-time highs. Comparatively, around $1.3 billion of Ethereum was traded. There’s quite a drop-off from there to Ripple, which saw $410 million change hands. But cryptocurrencies are already vastly more traded than conventional stocks. Apple trades roughly $4 billion a day in volume. For now, that remains ahead of the largest cryptocurrencies, but Bitcoin’s volume is knocking on the door. The higher trading volume of cryptocurrencies is one reason they fluctuate so drastically.

For traders, volume hints at sustainability of a given move. A drastic price increase with low volume might be fool’s gold. A drop with considerable volume behind it might mean a coin is in for an extended bear run. There are no certainties in cryptocurrency. But effectively assessing volume is an important tool in an investor’s belt.

InvestoPedia.com definition:

What is 'Volume':

Volume is the number of shares or contracts traded in a security or an entire market during a given period of time. For every buyer, there is a seller, and each transaction contributes to the count of total volume. That is, when buyers and sellers agree to make a transaction at a certain price, it is considered one transaction. If only five transactions occur in a day, the volume for the day is five.Volume as Indicator 'Volume':

Volume is an important indicator in technical analysis as it is used to measure the relative worth of a market move. If the markets make a strong price movement, then the strength of that movement depends on the volume for that period. The higher the volume during the price move, the more significant the move.

Fundamental analysis is based on company performance and is used to determine which stock to buy. Technical analysis is based on price and is used to determine when to buy. Technical analysts are primarily looking for entry and exit price points, and volume levels provide clues about where the best entry and exit points are located.

Volume Trends Confirm Strength:

Volume is one of the most important measures of strength for traders and technical analysts. Put simply, volume refers to the number of contracts traded. For any trade to occur, the market needs to produce a buyer and a seller. A transaction occurs when buyers and sellers meet and is referred to as the market price. From an auction perspective, when buyers and sellers become particularly active at a certain price, it means there is a lot of volume.Fundamental analysis:

is based on company performance and is used to determine which stock to buy. Technical analysis is based on price and is used to determine when to buy. Technical analysts are primarily looking for entry and exit price points, and volume levels provide clues about where the best entry and exit points are located.Volume Trends Confirm Strength:

Volume is one of the most important measures of strength for traders and technical analysts. Put simply, volume refers to the number of contracts traded. For any trade to occur, the market needs to produce a buyer and a seller. A transaction occurs when buyers and sellers meet and is referred to as the market price. From an auction perspective, when buyers and sellers become particularly active at a certain price, it means there is a lot of volume.Volume Analysts:

Analysts: use bar charts to quickly determine the level of volume. Bars also provide easier identification of trends in volume. When bars are higher than average, it is a sign of high volume or strength at a particular market price. In this way, analysts use volume as a way to confirm a price movement. If volume increases when the price moves up or down, it is considered a price movement with strength.